NDIS APR 2026-27: what it means for Allied Health Providers

The NDIA has released its Annual Pricing Review for 2026-27 and the new Pricing Schedule. The prices apply from 1 July 2026.

One thing that has changed this year is how they are published. In a normal year the NDIA releases the PAPL, the Pricing Arrangements and Price Limits, as the price list for the year. This year there is no new PAPL. The 2025-26 version ends on 30 June, and from 1 July the price list is a new document called the Pricing Schedule instead.

The reason is the Bill. The Securing the NDIS for Future Generations Bill would move the power to set NDIS prices to the Minister, with the NDIA advising. The formal price-limits document is on hold while that plays out. The Bill has not passed, and with the Senate inquiry now extended by eight weeks, passage is months away. It does not need to pass for the new prices to apply. The Pricing Schedule is the price list from 1 July, and it is what you bill against.

For some disciplines this is a significant change. Here is what moved, what sits underneath it and what to do before 1 July.

The price changes

Three therapy disciplines were cut.

Dietetics falls from $188.99 to $178.99, and Exercise Physiology from $166.99 to $161.99.

Other Professionals falls the furthest, from $193.99 to $156.16. That category bundled a wide range of services under a single price without identifying the practitioner's discipline at the point of claim, which meant the NDIA could not see what it was funding or benchmark it against anything comparable. The Schedule reduces the price, and the APR proposes identifying the practitioner's discipline at the point of claim to support future benchmarking, though that is a recommendation at this stage and no claim-level identification mechanism exists yet. Note: the reduction does not apply to Early Childhood supports delivered under this category, which remain at $193.99 (p.89).

Two disciplines increased. Psychology moves from $232.99 to $252.99, and Positive Behaviour Support (PBS) moves to the same $252.99 rate.

The largest group held at the same dollar figure: Occupational Therapy, Physiotherapy, Speech Pathology, Podiatry, Audiology, Social Work and Therapy Assistants. A held price is a reduction in real terms. Inflation, wages, rent etc. keep rising while the price does not.

Disability Support Worker (DSW) supports and core supports sit in a different bucket. They are indexed, so they will rise this year in line with the Fair Work Commission's 4.75% Annual Wage Review. Therapy is not indexed, which is why a frozen therapy price and a rising DSW price sit side by side in the one Schedule.

The new line items

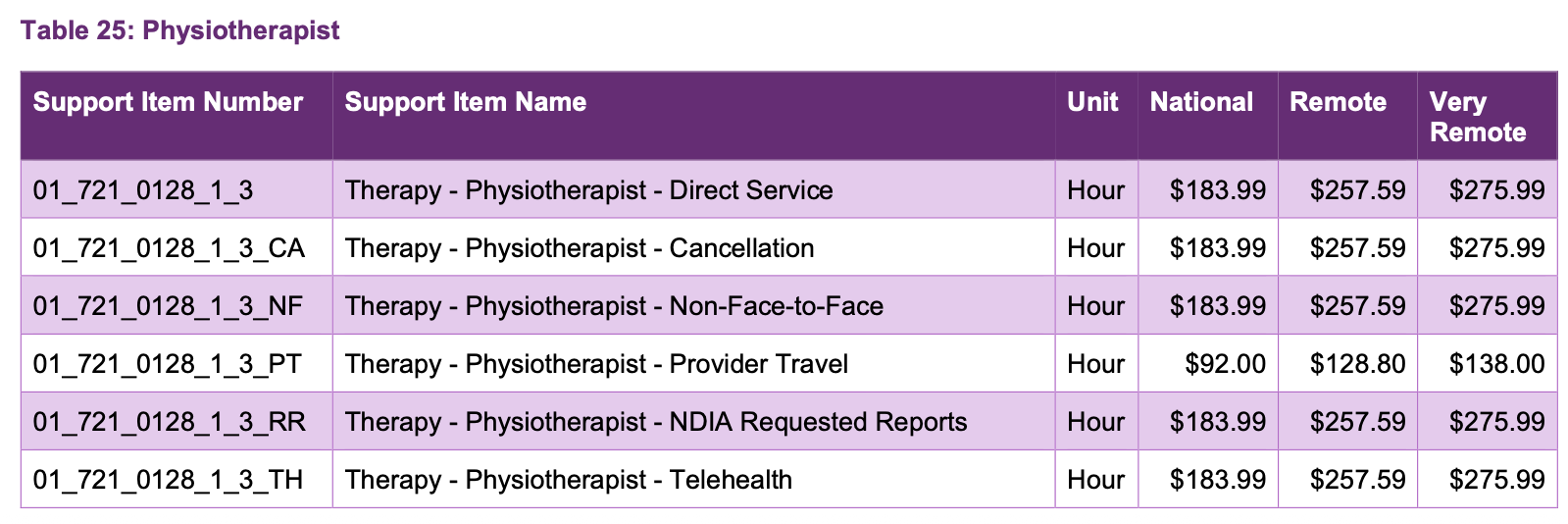

The change that will affect day-to-day operations most is structural. Each therapy discipline now carries six distinct line items: direct service, cancellation, non-face-to-face (NF2F), provider travel, NDIA requested reports and telehealth. See the new Physiotherapy line items below as an example:

Physiotherapist line items. Source: NDIA Pricing Schedule 2026-27, table 25, p. 36.

Provider travel sits at half the hourly rate, which is not new, since that cap came in last year. What is new is that travel, telehealth, report writing and NF2F time are now separated into their own line items rather than bundled, so each activity is identifiable in the claim data.

The reason this matters is data. Once each of those activities is visible as a separate line, the NDIA can see exactly how much of each is being claimed, by whom and in what proportion. The APR is open that this is the intent.

“session structure and transparency have become a policy issue in their own right"

NDIA, Annual Pricing Review 2026-27, p.94

This is where the practical questions start. A good deal of legitimate therapy work happens around the participant rather than directly with them, and the boundary between direct and NF2F time is not clearly defined. While everything is billed at a single rate the classification carries little financial consequence. The NDIA does not hold this data today, which is part of why the separation is being made. Once it does, the classification could start to carry financial weight, whether through differentiated pricing or other measures. Clearer guidance on where the line sits between NF2F and Direct Service would help, and hopefully it follows.

NF2F time deserves particular attention. Now that it sits as its own visible line, the volume and the method of NF2F charging are easy to read straight off the claim data. I can tell you that both the method and the amount of NF2F charging are under scrutiny by the NDIA. The risk sits in two places. The first is routine NF2F, billed as a matter of course rather than for genuine indirect work tied to a participant's goals. The second is overcharging, where a single session is loaded with an unreasonable amount of preparation, note writing, research, pack-down and travel.

In a tightening market the pull is to recover margin with travel and NF2F charges. Make sure you look at your own numbers first. Utilisation, operating model and internal costs are usually where the real margin sits, and improving them costs a participant nothing. I have written about this previously. If you do still want to increase your travel or NF2F billing, make it an informed decision.

Differentiated pricing, and where it is heading

The APR recommends differentiated pricing in one place this year. Social, Community and Civic Participation prices for unregistered providers would be cut by ten per cent from 1 January 2027, with indexation for that segment ceasing while registered providers are maintained (p.13). If adopted, this would be the first time registration status is used to set a differential price.

For therapy, the NDIA considered registration-based differentiation and set it aside this year. The review argues the existing method already accounts for differences in how supports are delivered:

"the benchmarking methodology already captures differences in delivery context"

NDIA, Annual Pricing Review 2026-27, p.33-34

That makes SCCP the test case for registration-based pricing. With this recommendation the NDIA has shown it is willing to price by registration status, and the open question is which categories it reaches next. Therapy is set aside this year, so a registration-based therapy price is not imminent. The direction is worth tracking, and much will depend on whether the SCCP change is adopted and how it plays out from January 2027.

It does sharpen a question providers already put to me, which is whether to register at all. With the two halves of the market now so far apart on price and scale, and mandatory registration expanding under the Bill for higher-risk supports, the decision carries more weight than it used to. The answer turns on your client mix, your risk profile and where you are taking your business.

For therapy, my read is that differentiated rates for telehealth and NF2F time are a likely next step, because face-to-face delivery costs more to provide than a phone call or a piece of report writing, and the new line items are how the NDIA will build the evidence. This sits squarely on the roadmap. The three-year pricing workplan places a Therapy Pricing Review in 2026-27, with differentiated pricing among its stated focus areas.

Support at Home shows what that separation can look like. The two schemes have sat in the one Government department since May 2025 and increasingly inform one another, with Support at Home a tightly consolidated sector while the NDIS is very much the opposite. Support at Home already splits Allied Health billing into direct and indirect units, with indirect time priced lower. However, unlike the NDIS, it does not allow travel to be billed separately, so that cost sits inside the direct rate. I work across both, and the structure is the part worth watching.

How the NDIA arrives at these numbers

It is worth understanding how the NDIA arrived at these prices.

DSW supports are indexed. Most disability support work is paid under the relevant award, so the price is tied to the cost of delivery and rises when the award rises. That is why DSW and core supports move with the 4.75% increase this year.

Therapy supports are benchmarked instead. The price is set by comparison against the Medicare Benefits Schedule, Private Health Insurance and other compensation schemes, on the basis that the same therapists move between all of these systems. The NDIS price is positioned to sit within the range of those external rates. That is why Psychology rose, because it sat below the range, and why Dietetics and EP fell, because it sat above it.

Why therapy is treated differently comes down to how therapists are paid. The HPSS Award sets a floor, and it covers only a minority of the therapy workforce. Most therapists are engaged under enterprise agreements or individual arrangements, with pay typically around 36 per cent above award rates (p.79). The NDIA treats those earnings as "contextual information rather than a pricing input" and concludes they are "an inappropriate basis for recommending prices" (p.79). So the award can rise, as it will this year, without therapy prices following.

Therapy prices are set from external market fees, so your own cost base does not enter the calculation. Understanding that matters, and what it means for the sector is a thread I will pick up properly in a separate article.

The market picture

The NDIA's Therapy supports section, from page 60, is worth reading in full. The data is the most detailed picture of the therapy market the Agency has published.

Therapy drew $2.7 billion in the six months to December 2025, around ten per cent of total Scheme spend. Over that period participant numbers grew 12.8 per cent while the number of active therapy providers fell 3.9 per cent.

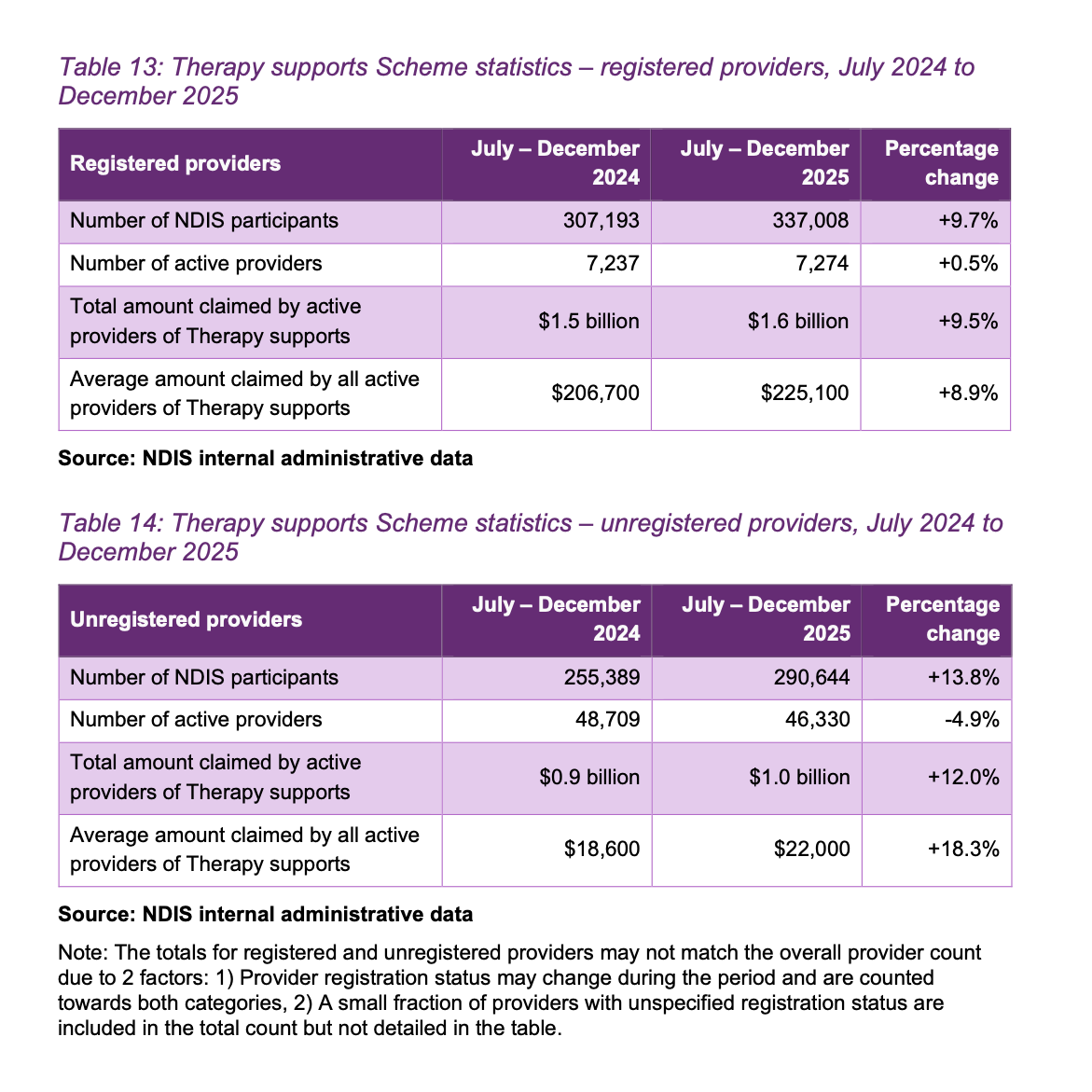

The registered and unregistered halves of the market are worth separating out:

Source: NDIA Annual Pricing Review 2026-27, Tables 13 and 14, p.64.

The shape of this is counterintuitive. Most therapy providers are unregistered, yet most of the money goes to the registered minority.

Registered providers number 7,274 and claim an average of $225,100 each over the six months, which comes to $1.6 billion. Unregistered providers number 46,330, around 87 per cent of the market, and claim an average of $22,000 each, splitting roughly $1.0 billion between them.

That tenfold gap in average claims describes two different populations. A small base of established registered businesses delivers most of the dollars, alongside a long tail of small unregistered operators, many of them sole traders. The fall in provider numbers sits almost entirely in that tail. Unregistered active providers dropped 4.9 per cent while the registered cohort held steady, which is the NDIA's basis for reading the decline as small operators leaving rather than a broad withdrawal.

The switching data points the same way. The review finds complete provider switching "relatively uncommon across all support categories" (p.30), with therapy at a 6.0 per cent complete switch rate that it puts down to people moving between modalities rather than disengagement.

Growing demand, a decline concentrated in small operators and low switching together form the NDIA's case that prices can come down (or stay the same) without driving providers out.

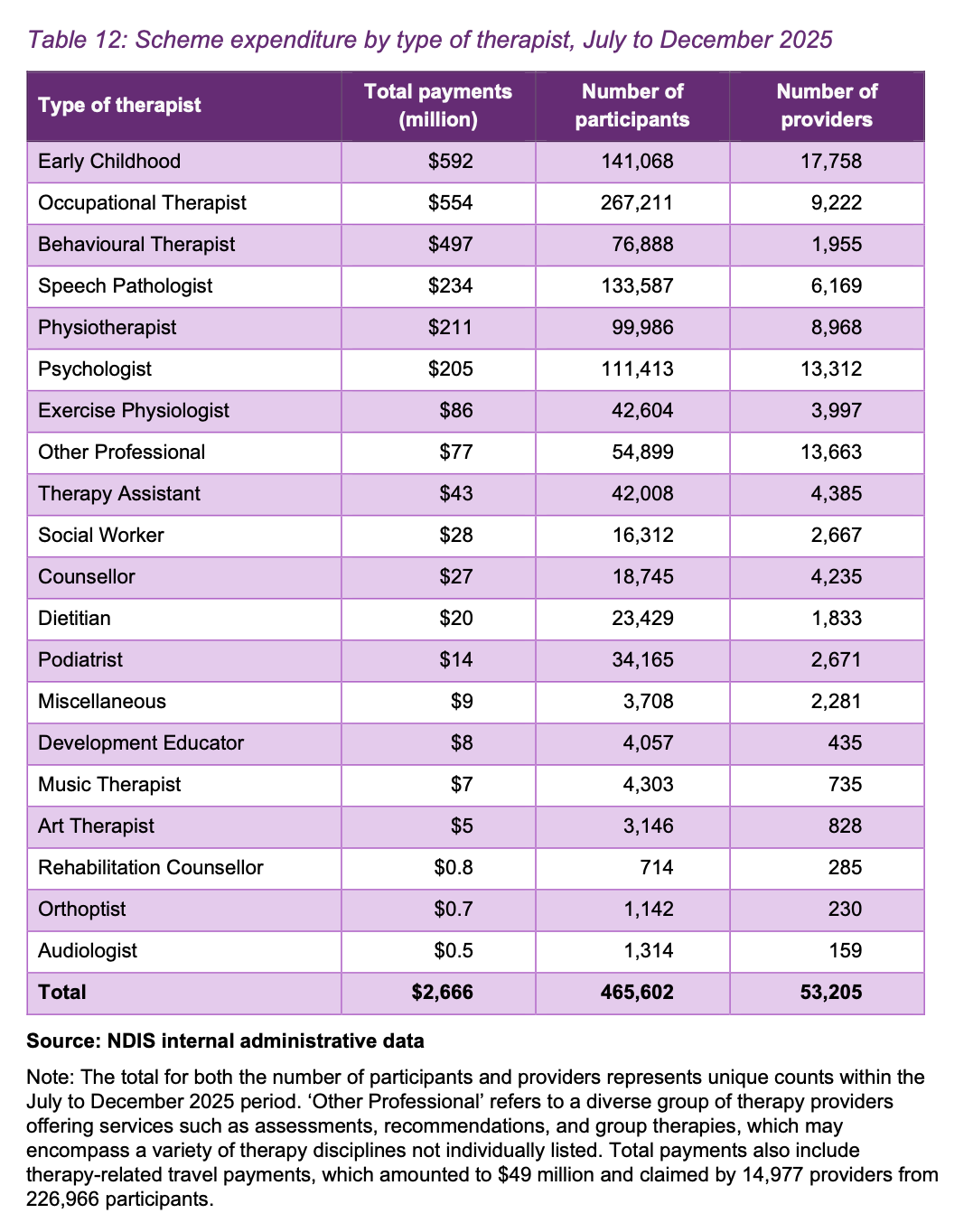

Source: NDIA Annual Pricing Review 2026-27, Table 12, p.63.

Spend is concentrated by discipline as well. Early Childhood is the single largest spend category and Occupational Therapy serves the most participants. The standout sits on a different measure. Behavioural Therapist, the PBS line, ranks third on spend and does it with only around 1,955 providers. That works out to close to $250,000 in payments per provider over the six months, against roughly $60,000 for occupational therapy. No other discipline comes close, and that gap sets up what follows.

One caveat sits inside these numbers. PBS is counted within therapy, and it is the one discipline where registration is mandatory, so every PBS provider is registered. That lifts the registered share of the therapy figures. Strip PBS out and the rest of therapy is more heavily unregistered than the headline suggests.

Behaviour Support is going to get more crowded

PBS runs against the falling-provider story. The rate has just moved to $252.99 and keeps climbing, while the conditions around entry are unusual.

For a provider, registration is genuinely hard. PBS is a specialist module, so a provider must hold certification, the far more complex of the two NDIS audit routes. Certification means the full core module plus the specialist standards, audited onsite every eighteen months. Most therapy providers never face that, sitting on light-touch verification or operating unregistered.

For an individual practitioner the bar is far lower. Entry is suitability-assessed against a capability framework rather than tied to a fixed qualification, so standards vary. Many practitioners also work under another entity's registration as subcontractors, capturing a high hourly rate without holding the registration themselves.

Put a rising rate next to a soft entry pathway (for practitioners), a subcontracting model and the highest revenue per provider in the market, and the pull into PBS is obvious. In the few hours since the APR released, clinicians and providers have already reached out to me about moving into PBS.

The participant-safety risk is higher here than any other therapy discipline in the scheme, which is why it sits as a certified specialist module. The safeguard lives in the registration pathway. The pricing signal, however, is pulling people in regardless. If you are weighing it, do not enter without proper governance and clear checks and balances, and treat certification as a floor rather than a ceiling. Do not move in for the rate alone.

Beyond therapy

Outside therapy the picture is steady for now. Support Coordination prices remain frozen, as they have been since 2019 (like a number of therapy prices). Plan Management holds its monthly fee at $104.45. Both sit ahead of larger structural change, with commissioning models for support coordination and a panel approach for plan management flagged in the Bill. The Isolated Towns arrangements also move to a two-tier model that better reflects how thin some of those markets are.

What to do before 1 July

Update your line-item codes. Every therapy discipline now has six codes: direct service, cancellation, NF2F, provider travel, NDIA requested reports and telehealth. Map your billing and practice management software to the current codes before 1 July, so claims do not reject and your NF2F and travel time is captured correctly.

Review your pricing and service agreements against the new Schedule. Confirm where you sit on each discipline you deliver, and check whether any agreements quote a dollar figure that has now changed.

Keep an eye on the Bill. It is before Parliament and not yet law. The Senate Community Affairs Legislation Committee was due to report on 23 June, but the inquiry has been extended by eight weeks to allow further scrutiny, with the report now due on 14 August 2026. That pushes any vote past the winter break, so the legislation will not pass before Parliament rises in early July as the government had intended. I will break the report down separately once it lands. A great deal of reform is attached to the Bill, including budget resets, commissioning of intermediary supports and an expansion of mandatory registration. This APR is one piece of a much larger program, and the timeline on that program has just lengthened.

If you want help working through what this means for your business, book a discovery call.

General commentary only. This does not constitute legal, financial, HR or compliance advice.